The C market, as of October 14th, is trading at $2.09/lb, back to the levels reached immediately following the frost in Minas Gerais and other coffee regions of Brazil this past July. This is in spite of nearly ideal rainfall patterns in Brazil. Drought no longer seems to be a primary concern, although it remains to be seen how trees stressed from frost will respond. Most forecasts have called for around a 10% reduction in the size of the 2022 Brazil crop. Increases in the NYC market have far outpaced such forecasts.

The primary reason for the current increase is a drawdown in certified stocks, the physical coffee which underpins the C market, in bonded warehouses at American and European ports. It is useful to think of certified stocks as a backstop for the coffee market. The larger they are, the greater the buffer in consuming countries against supply shortages. It also bears mention that the long-term trend is definitively negative. 10-15 years ago total global certified stocks regularly topped 4 to 5 million bags. Currently, they are below 2 million. Of even greater urgency is the rapid drawdown of 10-20% that has happened just in the past two weeks. Likewise, there are reports of contract defaults in Colombia as sellers renege on prior commitments in favor of a high spot market. Both of these events are symptoms of a high market. They also act as feedback loops which drive prices higher. Defaults create a perception of scarcity, increasing spot prices and causing certified stocks to decrease; lower certified stocks mean actual scarcity, driving spot prices still higher, potentiating further defaults. Differentials for Arabica coffee to be shipped during the first quarter of 2022 have not relaxed even a few cents, in spite of a 60 cent increase in the C market over the past three-and-a-half months. All of this is taking place against the backdrop of a global freight market which is still wildly disconnected from historically normal rates. The bottom line is that there are quite a few scenarios which will need to unwind themselves before any expectation of increasing supply buffers could be contemplated.

Normally, higher prices attract more deliveries to the board. With freight as expensive as it is and the ongoing spot tightness, the incentive is not there for a seller to deliver. What price does the C market need to reach in order for this equation to be rebalanced? It does not appear we are there yet. The scary thing is that until freight costs and differentials begin to relax, there may not be a “there” to be reached.

As always, there will be price corrections. There always are. The market retraced from 2.20 to 1.75 in seven trading days at the end of July. While speculating on coffee futures is not what any roaster really wants to be doing, it is imperative that you at least keep an eye on coffee prices right now. Talk to your Royal Coffee trader and come up with a plan for how much of an average price increase you can absorb. These scenarios are undeniably scary, but they need not be fatal if you are willing to make some tough decisions. 3-6 months of coverage bought and fixed right now is an absolute necessity.

-Max Nicholas-Fulmer

CEO

Royal Coffee

Latest Articles by Max Nicholas-Fulmer

Issuing IEEPA Tariff Credits to Our Customers

CBP has begun returning IEEPA duties on green coffee. Royal Coffee is now issuing IEEPA Tariff Credits to the customers who paid those tariffs.

What Does the Supreme Court Tariff Hearing Mean for Coffee?

The Supreme Court’s recent hearing on the IEEPA tariffs signals skepticism about presidential trade powers but no quick relief for importers. Refunds appear off the table, and tariff risk, especially...

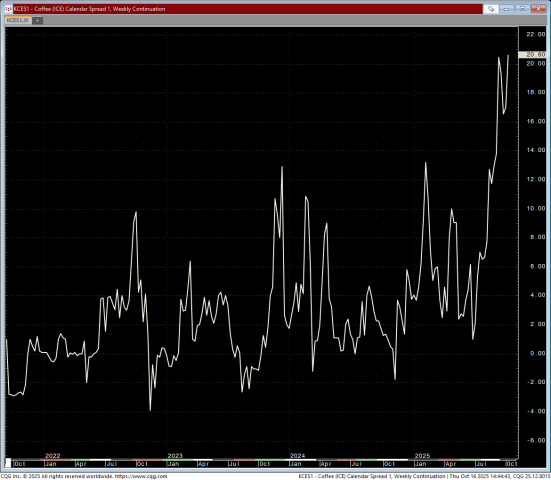

Coffee Market Update: Backwardation and What It Means for Roasters

The global coffee market has entered uncharted territory. Tight inventories, Brazil tariffs, and U.S.–Colombia trade tensions are pushing C-market prices higher and sustaining extreme backwardation. Learn what it means for...

How are farmers affected by the higher C price? Isn’t a higher C price better for them?