Article Summary:

- Global position: Niche specialty origin; ~0.8% of world production, ranked #15 globally.

- 2026/27 outlook: Production projected at 1.6 million bags; exports forecast at 1.41 million bags.

- Crop split: ~60% Arabica, ~40% Robusta, with Robusta growth driven by expanding farming in Kagera and Kigoma.

- Who grows it: ~450,000 smallholder farmers produce ~90% of the coffee; estates account for the remaining ~10%.

- Growing regions: Three macro-regions — West Lake Zone (Kagera, Kigoma), Northern Highlands (Arusha, Kilimanjaro; home to the Moshi auction), and Southern Highlands (Mbeya, Ruvuma).

- Harvest pattern: Bicyclical — lower-volume years often deliver higher cup quality due to more selective picking.

- Cultivars: Legacy Bourbons (e.g., TACRI’s N39), Kenyan SL-28 and SL-34, Kent, and K7.

- Peaberry niche: Tanzania is known in the US for peaberry (a single-bean anomaly in ~5% of coffee worldwide); AA and AB grades are also widely available.

- Export markets: Japan is the top destination ($58.4M green coffee in 2024), followed by the EU; US demand is rising.

- Logistics: Most coffee ships through the Port of Dar es Salaam.

- US timing: Arrivals begin November/December and peak January through March.

Tanzania Coffee Export Review 2026

A country of 73 million people, Tanzania is Africa’s most linguistically diverse nation with over 100 languages spoken within its borders. Its iconic landmark, Mount Kilimanjaro, is Africa’s highest peak, and its national parks (including the well-known Serengeti nature reserve and Ngorongoro crater) and safari lodges make the country a popular tourist destination.

Tanzania is expected to produce 1.6 million bags for the 2026/27 harvest. Coffee is the 6 largest commodity production in the country with peanuts, meal and sorghum taking the top three. Ranking #15 in terms of coffee production, it makes up 0.8% of the global production and is often considered a niche origin for green coffee buyers. To this day coffee (319M) is a major cash crop for Tanzania and is one of the top exports under gold (4.44B), coconut’s/Brazil nuts/cashews(629M), refined petroleum(602M), raw tobacco(500M) and dried legumes(450m).

Export Stats

Coffee sector is expected to expand in the coming years, largely due to the increase in robusta farmers in Kagera and Kigoma that are supported by subsidized seedlings and strong farm-gate pricing. Exports are forecasted to reach 1.41 million bags in the 2026/2027 year (compared to production at 1.6M). Continued interest in Tanzania’s premium arabica reinforce its position as a steady and high-quality coffee producing country in the international specialty market.

Coffee is mostly exported to the European Union and Japan, with U.S consumption on the rise. Japan is the top destination with $58.4 million spent on green coffee in 2024. Domestic consumption continues to rise in the 2025/2026 marketing year with expected consumption to rise hit an all-time high, 85,000 bags, up 9,000 from the previous year. This growth is driven by urbanization, expanding coffee culture and higher incomes. Tea still remains dominant in the country due to its affordability and cultural preference among consumers.

Production

With roughly 450,000 small-holder farmers they produce roughly 90% of the coffee from the country. Larger estates also exist in the country, and they make up the last 10% of the coffee grown. Of this production volume, around 60% is Arabica and the remaining is Robusta. Robusta is driving production and volume is up due to the bicyclical nature of the harvest volumes. Direct consumption is lower than other east African countries at 85,000 bags a year. Tourism and restaurant sectors make a huge contribution to this number and there is a growing urban coffee culture in Dar es Salaam and Arusha.

From 2019 to 2024 fields were rehabilitated and are now finally reaching full maturity which contributes to the expected increase in the following year. Stable prices over the years have supported coops which allow for more extensive support and training for producers. Unlike other countries, Tanzania has experienced favorable rainfall and steady temperatures that have supported growing conditions.

Harvest seasons in the country are bicyclical, every two years there is a larger harvest, this impacts quality and pricing. During a low volume harvest cycle, you can expect higher cup quality due to less cherry to sort through, leading to better picking and better quality.

In 2023 Tanzania Coffee Board had already distributed 13 million improved seedling to farmers and by 2025 they have a goal of distributing 25 million by 2025 according to a USDA annual report. Seedlings support growth of existing coffee farms rather than establishing new plantations, this would make sure the harvested area stays the same but supports productivity.

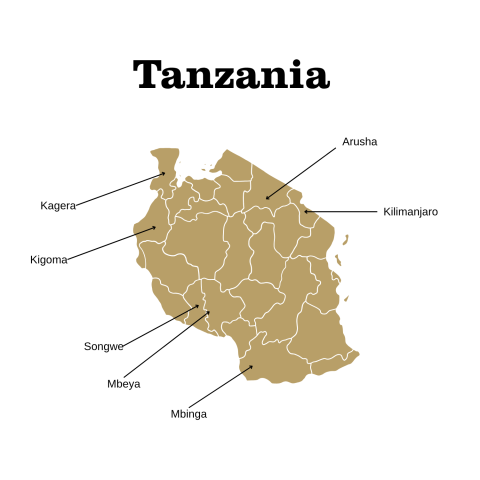

Growing Regions

There are three primary macro-regions of Tanzania where coffee is grown. In the northwest along the border with Uganda, Rwanda, and Lake Victoria, we see coffee in the West Lake Zone, often designated as Kagera, the name of the primary administrative region in the area. Coffee also grows a little further south in the Kigoma region near the border with Burundi near Lake Tanganyika.

The Northern Highlands represent coffee grown in the Arusha and Kilimanjaro administrative regions. With a higher percentage of estate coffee in the area, and often set against the indominable backdrop of Mount Kili, these are often the most recognized sources of Tanzanian beans to international buyers. The town of Moshi, which hosts the coffee auction, rests in Kili’s southern foothills, while coffee grown west of Mount Meru and Arusha town, in districts of Karatu and Oldeani, border the safari destinations of Lake Manyara and the Ngorongoro crater.

Tanzania’s Southern Highlands spans a much wider reach of geography in the country’s agricultural heartland bordering Malawi, Zambia, and Mozambique. Coffee grown in the largely rural administrative regions of Mbeya and Ruvuma is primarily harvested and processed by smallholders and cooperatives, and production here has largely increased in recent years. Recognizable coffee producing districts include Rungwe, Mbozi, and Ileje within Mbeya, and Songea and Mbinga in Ruvuma.

Cultivars

In much of the country, older legacy Bourbons often dominate the arabica-planted smallholder plots and estates alike. One of the more popular iterations of this cultivar is TACRI’s N39 variant.

Kenyan cultivars have made their way south across the border to Tanzania, including the older SL selections like SL-28 and SL-34, in addition to newer hybrids like Ruiru-11 and Batian.

SL-28, while typically thought of as Kenyan in origin, was in fact first selected in Tanzania. It is a well-known cultivar in Africa and has a very good reputation for cup quality and resistance to drought. It does not fare well against major diseases in coffee but for the most part is durable and notable for its rusticity. The plant can be left alone for a few years but return to successful harvest production levels. Scott Agricultural Laboratories initially selected the cultivars and was a Laboratory that was established by the British government in Kenya in 1920’s.

Perhaps the other most common arabica varieties in Tanzania are Kent and K7, which are sometimes are conflated but are distinct tree types.

Kent is a century-plus-old selection originally from India, where it was chosen for its leaf rust fungus resistance as early as 1911. (It is frequently listed as a Typica-related tree, but World Coffee Research lists it as likely Bourbon related). Kent is no longer considered rust resistant, nor is its sub-selection KP423, which can be found commonly in nearby Uganda as well.

K7 is found throughout Kenya and Tanzania and is tolerant to coffee leaf rust and coffee berry disease. Quite large beans, they have a high yield potential and is considered to have good cup quality at high altitudes. Created by Scott Laboratories and released in 1936 in Kenya, it is still widely planted throughout the region. Genetic tests have confirmed the cultivar is related to the Bourbon genetic group.

The peaberry is not technically a cultivar, but a genetic anomaly in coffee. An average coffee fruit contains two seeds (beans), while a peaberry contains just one. Some people claim the flavor is more concentrated, but there’s no definitive proof of this as a universal principle. Peaberries typically occur in about 5% of all coffee worldwide, regardless of plant type or origin.

Tanzania, for whatever reason, has carved a niche in the US market for peaberry. If you had a coffee from Tanzania roasted in the United States in the last two decades, chances are high it was a peaberry. It’s quite likely that the bean type was used in early origin-marketing to second and third wave roasters as a way to differentiate Tanzanian coffee from its occasionally higher-profile neighbor, Kenya.

Logistics

The main port of the country is in the city of Dar es Salaam called the port of Dar es Salaam. One of three ports in the country, it handles more than 90% of the cargo traffic. Not only it is an important port for Tanzania but for six landlocked countries surrounding it as well. Main alternative ports exist in Tanga on the north Indian Ocean coastline, and Mtwara in the south.

Most of the coffee production happens on the west side of the country, on the border of the Republic of Congo. Coffee has to travel all the way across the country to reach the port of Dar Es Salaam. Lots of roads to cover in areas that don’t the support of infrastructure can come into challenging circumstances to move it without damaging the coffee.

Royal Coffee Availability:

Coffee from Tanzania to Royal comes in smaller quantities and the same is true for most other importers. Just this week (6/15), we have five crown jewels arriving from Tanzania along with a larger lot available. Some of which are from a producer that we buy from year after year – Neel and Kavita Vahora are a brother and sister duo that have the taken generations of family knowledge and have turned it 1000 acres to a coffee enterprise. Be sure to check out our Crown Jewel offerings to see the latest Tanzania coffees available.

There seems hardly enough peaberry produced in Tanzania to meet demand. While Royal stocks large quantities of peaberry, we have equally-nice tasting coffees in AA and AB grades as well, and would encourage you to give them a try if your favorite PB grade isn’t available.

Tanzania lies just south of the equator and can generally be expected to harvest coffee, as with other regions, during its hemispheric winter. However, with hundreds of miles separating the country’s northern growing zones from those in the south, regional asymmetries in harvest timelines can be more exaggerated than countries with less geographical distance.

The Southern Highlands regions will typically begin picking cherries as early as May and continue as late as September in some cases. In the north, these timeframes can be somewhat delayed. Moshi, Kilimanjaro, and Arusha usually harvest June through August, while coffees grown around the Ngorongoro crater might not be finished with their last pass until late November.

Regional auctions usually begin in August in the south, followed shortly by those in the north, and may continue through the early months of the following calendar year. In the United States, arrivals might begin to trickle in during November and December, and typically peak January through March with later arrivals landing during the early summer.

Latest Articles by Isabella Vitaliano

Brazil Export Review

Brazil dominates 40% of global coffee production, but 2026 brings arabica declines, record-high prices, and climate pressures. Royal Coffee's 2026 export review covers production forecasts, key growing regions, cultivar profiles,...

Ecuador Coffee Export Review: Loja, Zamora Chinchipe & Pichincha

Article Summary: This article is a green coffee export review of Ecuador written for specialty coffee buyers and importers. Key topics: Ecuador produces roughly equal volumes of Arabica and Robusta,...

What Does ‘Direct Trade’ Actually Mean? A Specialty Coffee Reality Check

By Isabella Vitaliano and Chris Kornman Article Summary Direct Trade originally popularized by specialty roasters in the late 1990s to improve transparency and relationships with producers, the term suggests direct...