Wild gyrations in the coffee market, and how to cope.

If you’ve been watching the coffee market recently, you are doubtless aware of the massive decline in coffee futures prices on the Intercontinental Commodity Exchange (“ICE”, colloquially still known as the “New York ‘C’ Market,” or just “the C”). Since peaking at $2.30/lb on September 26th, the market for December Delivery closed today at $1.6980, a decline of nearly 25% in a single month). With an even wider lens, the market has traded between $1.05/lb and $2.55/lb in the space of 24 months. A global pandemic and the snarled logistics situation that followed, coupled with a real and damaging frost in Brazil in July of 2021, gave us a full year of the “C” trading above $2.00/lb. This is only the fourth time in history that prices have remained elevated above this level for this amount of time, and only the second time since the mid-1980’s. This translated through to record parchment costs in places like Colombia, along with unprecedented cherry prices in Ethiopia during 2021. Now, highly beneficial and well-timed rains in Brazil throughout September and October have led many agronomists to predict a bumper crop during the next “on-year” harvest cycle, approaching a combined Arabica and Robusta figure of 73 million bags from the world’s largest producer. Anecdotal availability of seedlings for coffee nurseries throughout Brazil is extremely limited, indicating just how much planting farmers have done to take advantage of the higher futures prices many have been able to lock in. We have seen a lot of things over the years, but never an elevated C market in the face of a surplus from Brazil. Combine this with a very strong US dollar as a result of rising interest rates, along with global recession concerns, and the market has clearly entered a structural readjustment phase.

If we look at the monthly continuation chart below, a couple things stand out. The frost I mentioned took place during the first weeks of July, 2021. The market started from a level of $1.55/lb prior to the frost, about 15 cents below today’s close. Likewise, the 200 week moving average, represented by the black line, now sits just below $1.51. While it would be foolish to predict, these levels may act as sign-posts for buyers seeking a bit of guidance on price direction.

If you are familiar with our offering sheet, you will have noticed coffee for 2023 shipments starting to appear. The harvest is underway in the lower altitude areas of Central America, Colombia is in full swing, and East Africa is beginning to ramp up as well. You’ll be seeing quite a bit more coffee to book forward over the next 6-8 weeks. With prices having fallen, we recommend taking advantage by ensuring that you have coverage at least until mid-Spring. The very earliest shipments from Central America, for example, will get out in late December and January, arriving to destinations likely by mid to late February. These early shipments always sell out fast and our spot position, while ample, will certainly be drawn down further before they arrive.

Forecasting out through 2023 is a bit murkier, but as always the best way to approach coffee buying is to avoid the temptation to try to be 100% correct and “call the bottom.” Buy a good chunk of coffee now, perhaps leaving some of it “unfixed” to take advantage of a further drop in prices. The closer we get to the long term average in the 150’s and below, the higher percentage of inventory you should have bought and fixed. Make sure you are talking to your trader as they can help guide you through this process and make recommendations on the timing of arrivals, and which coffees you may need to book heavier to get into the new crop arrivals season.

Latest Articles by Max Nicholas-Fulmer

Issuing IEEPA Tariff Credits to Our Customers

CBP has begun returning IEEPA duties on green coffee. Royal Coffee is now issuing IEEPA Tariff Credits to the customers who paid those tariffs.

What Does the Supreme Court Tariff Hearing Mean for Coffee?

The Supreme Court’s recent hearing on the IEEPA tariffs signals skepticism about presidential trade powers but no quick relief for importers. Refunds appear off the table, and tariff risk, especially...

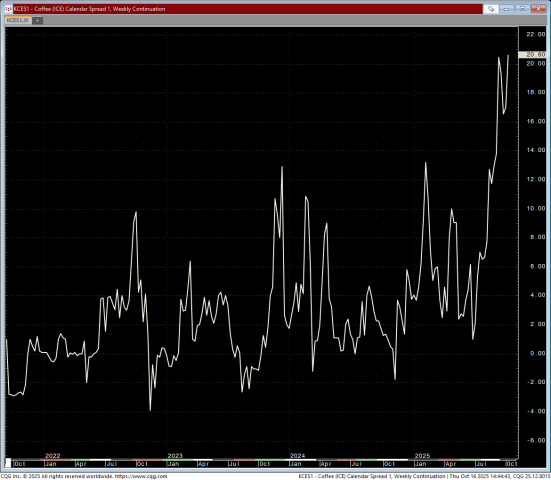

Coffee Market Update: Backwardation and What It Means for Roasters

The global coffee market has entered uncharted territory. Tight inventories, Brazil tariffs, and U.S.–Colombia trade tensions are pushing C-market prices higher and sustaining extreme backwardation. Learn what it means for...